Egypt Downgraded To ‘B-‘ On Mounting Funding Pressures; Outlook Stable

- Slow progress on key monetary and structural reforms has delayed the disbursement of multilateral and bilateral funds critical to covering Egypt’s high external funding needs.

- The costs of delay include a foreign currency shortage, a wide gap between the official and informal exchange rates, lower remittance inflows, and weaker private sector confidence and growth.

- We therefore lowered our long-term sovereign credit rating on Egypt to ‘B-‘ from ‘B’ and affirmed our ‘B’ short-term rating. The outlook is stable.

Rating Action

On Oct. 20, 2023, S&P Global Ratings lowered its long-term foreign and local currency sovereign credit ratings on Egypt to ‘B-‘ from ‘B’. The outlook is stable. We also affirmed our short-term sovereign credit ratings at ‘B’

At the same time, we revised downward our transfer and convertibility assessment on Egypt to ‘B-‘ from ‘B’.

Outlook

The stable outlook balances the risk that the Egyptian authorities may be unable to finance high external debt redemptions or address the country’s foreign currency shortage against the possibility of an acceleration of key monetary and economic reforms that would help bridge Egypt’s large external financing gap.

Downside scenario

We could lower the ratings if the authorities fail to implement the macroeconomic reforms required to reduce Egypt’s economic imbalances and to unlock multilateral and bilateral funding.

We could also lower the ratings if the government’s already elevated interest costs rise further, increasing the risk of a distressed debt exchange.

Upside scenario

We could raise our ratings if Egypt reduces net government debt levels and gross external financing needs, via an acceleration of reforms that support competitiveness, growth, and fiscal outcomes. Under such a scenario, we would expect renewed bilateral and multilateral financial support.

Rationale

The downgrade reflects the recurring delays to the implementation of monetary and structural reforms, exacerbating imbalances in the currency market, deteriorating the net foreign asset position of systemic banks, and delaying critical IMF disbursements and other multi- and bi-lateral financing. These funding sources include Gulf Cooperation Council (GCC) support, which we expect to continue. That said, given the evolution in the nature of GCC funding toward greater conditionality and achieving economic returns, we have less confidence that additional financing will be forthcoming in a timely manner to cover all external funding gaps.

We also view the government’s very high debt servicing costs, which largely relate to its domestic debt (70% of the total), as a potential challenge to debt sustainability. Interest spending consumes over 40% of government revenues, limiting fiscal space to provide additional support to Egyptian households grappling with a severe, multi-year cost of living crisis. The financial strength of Egypt’s large commercial banking system–with total financial assets at about 130% of GDP–is highly correlated with that of the state. We estimate banking sector gross claims on the general government, including securities and credit facilities, are equivalent to 60% of total assets.

Furthermore, limited transparency around the financing sources and import content of ongoing “national projects,” constrains our ability to assess their implications for public sector debt and the balance of payments.

Despite an agreement with the IMF to move to a flexible exchange-rate system, the government’s response to currency pressures has been to impose controls on private sector imports, via the banking system. With presidential elections scheduled to take place in December, policymakers are understandably preoccupied about the second-round effects of a devaluation on inflation. Moreover, the authorities may be aiming to increase reserve buffers ahead of any exchange-rate adjustment to help smooth post-liberalization volatility. While such concerns are understandable, in our view, the costs of delaying exchange-rate liberalization are also high and rising. These include a reduction in badly needed remittance and investment inflows, alongside weaker private sector confidence.

We expect an exchange-rate adjustment will result in a devaluation of the Egyptian pound (EGP) to around its level in the parallel market, currently about EGP40 per U.S. dollar. After which, we expect the Central Bank of Egypt (CBE) to allow the pound to be much more responsive to external shocks. That said, given the economy’s high import dependency, and the political sensitivity of inflation, in our view, the authorities may be tempted to re-introduce foreign currency controls as they have done previously, should currency volatility worsen.

Higher inflation will likely result in higher CBE policy rates, further increasing government debt service costs, at least in the short term.

On Oct. 7, the Palestinian group Hamas attacked Israel. In response, Israeli air strikes have targeted Gaza and Israeli troops are preparing for a ground invasion. Thousands of people have died on both sides. It is unclear how the conflict will develop. Our current base case is that the conflict will likely be largely contained to Israel and Gaza (see “War In The Middle East Compounds Global Geopolitical Risks,” Oct. 18, 2023). However, given its border with Gaza, and its control of the Rafah crossing, Egypt is directly affected. The shutdown of Israel’s Tamar gas platform has already reduced Egypt’s gas imports to 650 million cubic feet per day (cf/d) from 800 million cf/d, reducing Egypt’s ability to meet domestic demand and export liquefied natural gas. As a result of the conflict, Egypt is also likely to see fewer tourists, further pressuring the Egyptian economy, in our view.

Institutional and economic profile: Implementation of reforms, including the reduction of the state’s economic footprint, are key to Egypt’s economic prospects

- We expect President Al-Sisi to be re-elected in December 2023 and lead the government in its pursuit of the key tenets of the IMF program.

- The government has begun to sell stakes in state-owned enterprises (SOEs) to develop the private sector and encourage foreign direct investment (FDI) inflows rather than more flighty portfolio investment.

- We expect Egyptian economic growth to average about 4% over the next three years, albeit these forecasts will remain highly sensitive to exchange-rate and inflation trends, as well as to the fallout on tourism from the Israeli-Hamas conflict.

In our view, the presidential elections were brought forward to December 2023 from spring 2024 to create political space to enable the authorities to implement post-electoral reforms. The incumbent, Abdel Fattah Al-Sisi, is widely expected to retain his position after presidential elections to be held from Dec. 10 to Dec. 12, 2023. The results are likely to be announced on Dec. 18. If a run-off election is required, the results will be announced on Jan. 16, 2024. Constitutional amendments in 2019 allow candidates to run for a third presidential term and extended term lengths to six years from four.

Key structural constraints to economic growth include the large informal sector; relatively weak, albeit improving, governance and transparency of SOEs; and barriers to competition that restrict private-sector activity. As part of the conditionality of the IMF program, the government is implementing a law to improve the business environment by ending preferential tax, fees, and customs treatments for the economic and commercial activities of SOEs including military companies. The CBE has also discontinued its subsidized lending programs.

The government has embarked on a plan to reduce its dominance, and that of the military, over much of Egypt’s productive sectors. In December 2022, President Abdel Fattah Al-Sisi outlined the government’s vision for the future role of the state in the economy. This included raising the participation of the private sector in public investments to 65%, from 30% currently, within three-to-five years. The government has made progress selling stakes in various SOEs, meeting its target for fiscal year 2023 (ended June 30, 2023). The related U.S. dollar inflows to the country of about $2.5 billion are gradually being released, following due diligence by the investors. As a result, FDI inflows increased to nearly $10.0 billion in fiscal 2023, the highest level on record. We expect FDI to remain around this level in fiscal 2024. The government is working on a further $4.6 billion in asset sales this year.

We estimate economic growth slowed to about 4.0% in fiscal 2023, from 6.6% in the previous year. The lack of foreign currency availability restricted imports, which depressed economic activity, particularly investment. The cost and apparent preference of national project investments–with elevated import content and an uncertain productive benefit to the economy–has raised questions about Egypt’s economic strategy, and the extent and sources of extra-budgetary financing. However, we understand that the government has issued a decree, whereby projects with a completion rate of 50% or below, or with a heavy foreign currency component, are to be stopped. This should reduce related imports and support the external position.

In fiscal year 2023, tourism revenue on the balance of payments reached a record high of $14 billion, supported by Egypt hosting the 2022 United Nations Climate Change Conference, more commonly referred to as COP27. A sharp decline in tourists from Russia and Ukraine was more than compensated by a pickup in tourists from other countries, including Germany and Italy.

The tourism sector is an important source of foreign currency earnings for Egypt. However, given the uncertainty around the exchange rate, we understand the associated foreign currency inflow for the most part has been kept by commercial entities rather than flowing through the financial system. As a result, there is relatively limited availability of foreign currency on the interbank market.

Due to the foreign currency crunch, we expect GDP growth to slow further in fiscal 2024. However, after the CBE’s long-term strategy for the exchange rate becomes clearer, market confidence should improve. We project growth to pick up over our forecast horizon to fiscal 2026. The construction and energy sectors could be key drivers of growth, along with IT and communications, wholesale and retail trade, agriculture, and health care. The Hayah Karima program, which aims to improve living standards in rural communities, should help develop the quality of infrastructure.

The sociopolitical environment in Egypt remains relatively fragile, in our view, with about 30% of Egypt’s 105 million population below the poverty line. Sporadic small-scale protests reflect the discontent of more vulnerable and younger sections of society. The 2011 political uprising, which unseated long-time president Hosni Mubarak, was partly spurred by high unemployment and food price inflation. Under the existing subsidies program, more than 60 million Egyptians, or nearly two-thirds of the population, get five loaves of round bread daily for 50 U.S. cents a month; this has barely changed since countrywide bread riots prevented a price hike in the 1970s. Given these political dynamics, the government largely covered the cost of higher wheat prices in 2022 and postponed a reform to the bread subsidy scheme. In response to very high inflation, the government has also implemented wide ranging social support programs, including widening the number of households benefiting from the Takaful and Karama schemes, doubling the exceptional allowance for pensioners, and increasing the minimum wage for public servants. This was achieved within the confines of the government’s fiscal targets.

Egypt will become a full member of the BRICS group of countries (comprising Brazil, Russia, India, China, and South Africa), from January 2024. We do not expect this to significantly boost the economy (see “Broadening BRICS May Have Limited Economic Benefits,” published on Sept. 5, 2023). Egypt has had access to concessional funding from the BRICS-created New Development Bank (NDB; AA+/Stable/A-1+/) since 2021.

We expect GCC states to continue to support Egypt, given that instability in the country could spill over into the rest of the region. A matter of weeks after the onset of the Russia-Ukraine conflict in February 2022, when it became clear that Egypt would experience financial stress, some GCC states deposited $13 billion (2.7% of Egyptian fiscal 2022 GDP) at the CBE.

However, GCC states have recently been directing their funds to Egypt via more commercially focused routes, for example by purchasing stakes in SOEs. This is an alternative to providing substantial funds without conditions on concessional terms. We expect the GCC to provide more commercially oriented support, such as the United Arab Emirates (UAE) dirham (AED) 5 billion ($1.36 billion equivalent) currency swap, announced in September, between the CBE and UAE central bank. This allows Egypt to finance trade with the UAE, up to the prescribed amount, in EGP rather than U.S. dollars. The CBE also has the equivalent of a $2.6 billion (0.7% of GDP) swap line with the People’s Bank of China. In August, UAE entities also announced a $500 million package of low-cost financing to support Egyptian wheat purchases, $100 million per year (about 0.1% of GDP each year).

Tension with Ethiopia largely relates to the Grand Renaissance Dam, although under our base-case scenario we do not expect there to be a significant escalation. Ethiopia continues to fill the reservoir behind the dam, raising concerns over water shortages in Egypt and Sudan, which also depend on the Nile’s waters. Ethiopia is filling the reservoir to power a turbine and increase electricity provision in the country. To mitigate the risk, Egypt is directing more water from Lake Nasser, the reservoir behind its own hydropower Aswan High Dam, into the Nile, and implementing several desalination projects and water management strategies, such as recycling agricultural waste and surface water.

Flexibility and performance profile: Increased exchange-rate flexibility should keep current account deficits moderate

- Egypt’s current account deficit narrowed sharply in fiscal 2023.

- The fiscal 2023 government deficit was lower than we expected but is budgeted to widen this year.

- Inflationary pressures are likely to remain high as we expect further exchange-rate weakness.

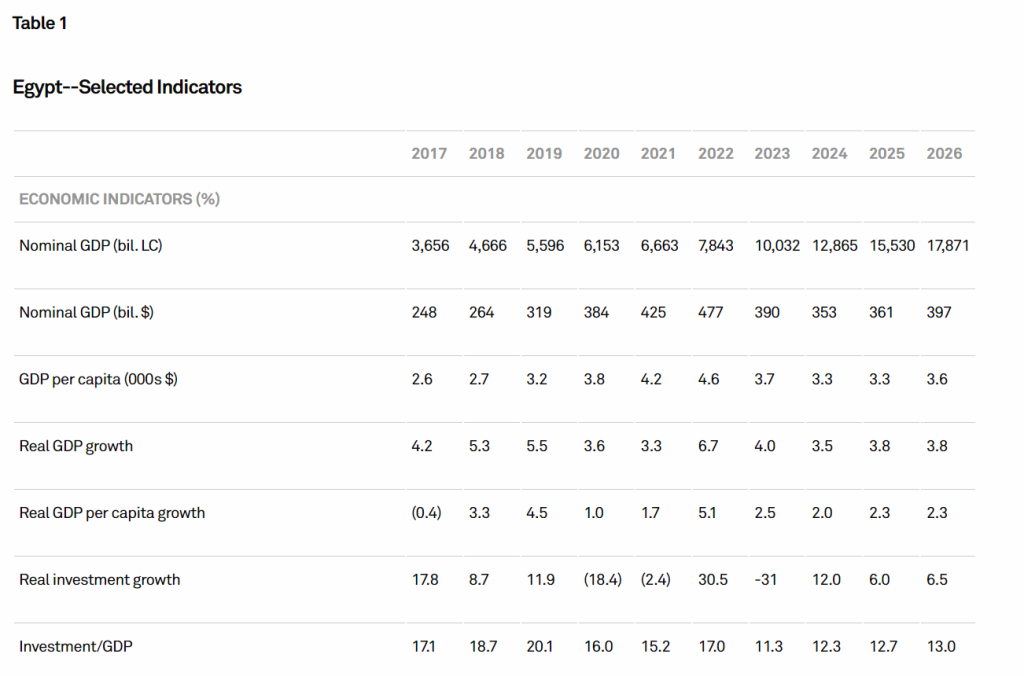

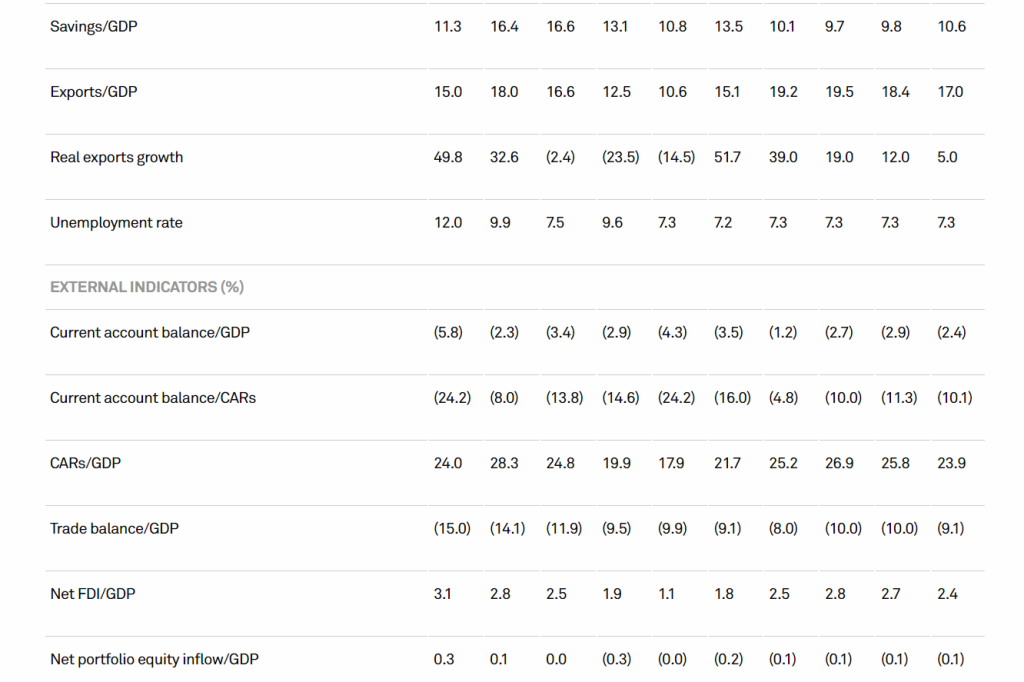

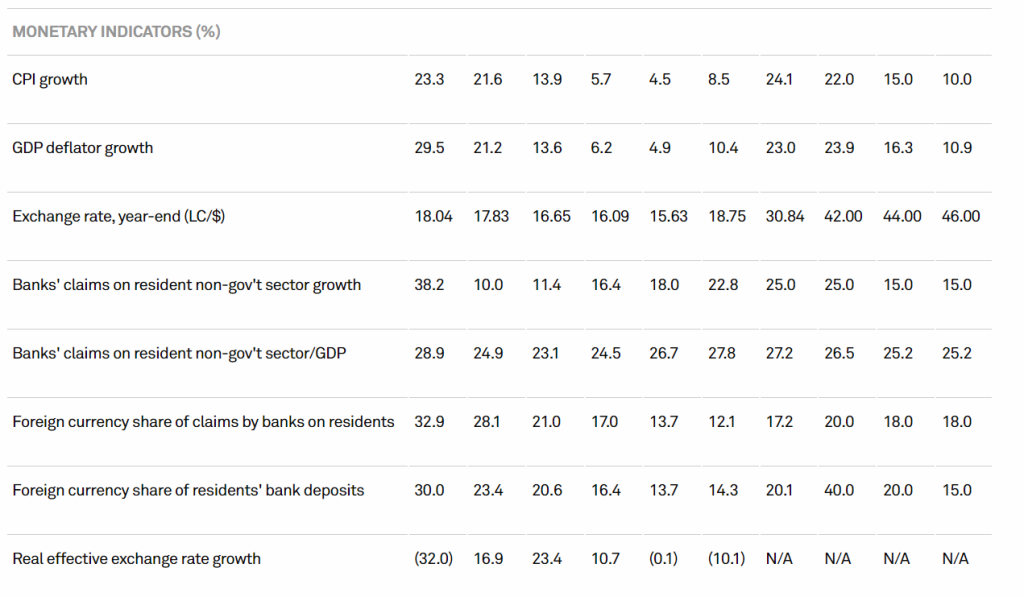

Egypt’s current account balance is broadly characterized by a large deficit on the goods balance, alongside a deficit on net income, which the surpluses on the services and transfers balances are insufficient to offset. The lack of foreign currency has led to a sharp contraction in goods and to a lesser extent services imports. This was the main reason for the narrowing of the current account deficit to $4.7 billion (1.2% of GDP) in the fiscal year ended June 30, 2023, from $16.6 billion (3.5% of GDP) in fiscal 2022. The high level of tourism and Suez Canal-related revenues also supported a strong performance by service sector exports.

We expect a resolution to the current foreign currency crunch to allow imports to grow and remittances to strengthen over the forecast period to fiscal 2026, resulting in wider current account deficits, which we expect to average 2.7% of GDP. This is lower than the current account deficits in the three years to fiscal 2022, which averaged 3.6% of GDP, because we think increased exchange-rate flexibility and a depreciating currency will constrain imports and support exports.

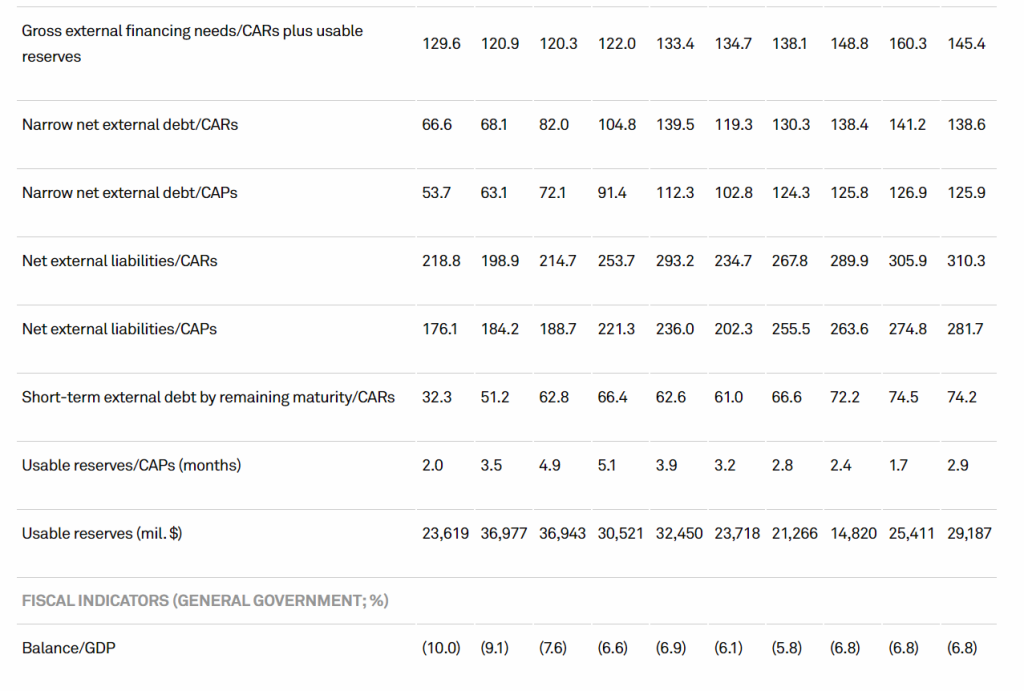

In terms of external funding, we expect net flows to the financial account will more than offset the current account deficits over the period through fiscal 2026, with CBE’s gross reserves rising to $38 billion on average. We expect Egypt’s net external debt, adjusted for liquid external assets, to average about 139% of current account receipts (CARS) over the period through fiscal 2026. The CBE is not intervening to provide foreign currency to the domestic economy and, as such, its international reserves have been gradually increasing. Instead, commercial banks’ balance sheets have taken the hit as they liquidate foreign assets and increase borrowing from abroad, while households and companies have limited access to foreign currency via official channels.

Given the short-term nature of the inflow of GCC deposits in fiscal 2022, our external liquidity metric has deteriorated. We estimate gross external financing needs as a share of CARs and usable reserves of about 150% over the three years through fiscal 2026, and usable reserves covering about 2.4 months of current account payments over the period until fiscal 2026. Our estimate of usable reserves deducts required reserves on resident foreign-currency deposits from officially reported reserves. Given the uncertainty about the level of the EGP, we expect foreign currency deposits, and therefore required reserves, to increase sharply to 40% of total deposits in fiscal 2024, having reached about 20% in fiscal 2023.

In addition to funding of the current account ($9.5 billion) in fiscal 2024, we estimate principal payments of about $8 billion on government external debt (for the whole economy principal payments are about $19 billion). Payments to multilateral agencies account for 67% of the government’s principal payments on external debt in fiscal 2024, with the IMF alone accounting for 48% of the total. We expect most of this donor funding to be rolled over on concessional terms. About $2 billion, or 27%, relates to the government’s principal payments on commercial external debt. Interest payments on external commercial debt are an additional $2 billion. We expect this commercial debt service to be made on time and in full.

About 70% of Egypt’s government debt is domestic and in local currency. The main funding source for this domestic debt is the Egyptian banking system, which, in our view, remains liquid in local currency and can increase its lending to the government, if necessary, despite its already-high exposure at about 60% of total assets. This is because we think the banking sector has solid domestic liquidity in local currency, with a low loan-to-deposit ratio at 48.7%, as of April 2023. Resident deposit growth is high, averaging above 20% annually over the three years to fiscal 2022. This is partly due to rising levels of financial intermediation, as the base of financial inclusion in Egypt is very low. We estimate that Egyptian domestic banks–of which the two state-owned banks, National Bank of Egypt, and Banque Misr, constitute close to half in terms of total assets–hold about 60% of general government securities. The CBE holds another 10% of the total.

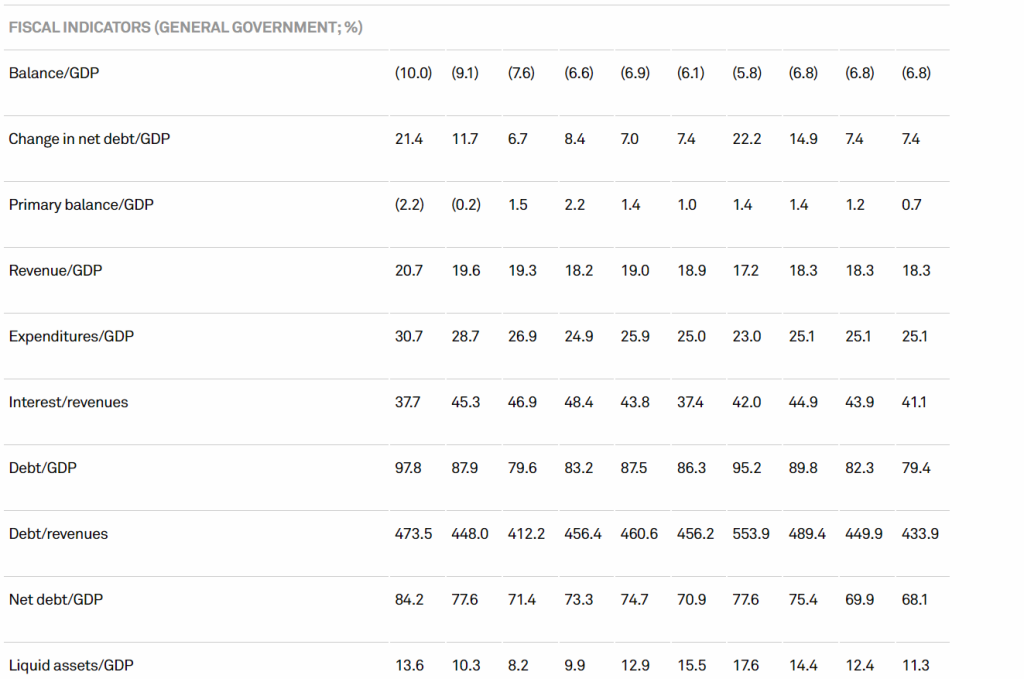

We estimate that the general government deficit will rise to about 7% of GDP on average, over the period through fiscal 2026, having narrowed to 5.8% in fiscal 2023 due to strong revenue growth. We estimate that even amid the current challenges, the central government primary surplus (deducting interest costs from the headline deficit) will average about 1% of GDP over fiscals 2024-2026, similar to the level reported over the previous three years. However, we note that the government is targeting a primary surplus of 2.5% in fiscal 2024, suggesting some upside to our fiscal forecasts. We expect tax administration reforms and a broadening of the tax base to strengthen the fiscal balance. On the spending side, growth will be spurred by capital investments, subsidies, grants, social benefits, and salaries.

Headline inflation is well above the upper boundary of the CBE’s target range of 7% plus or minus 2%, partly as food prices, which had been increasing even before the Russia-Ukraine conflict, continue to rise. Inflation has been gradually rising since mid-2021 and reached 38% in September 2023. The CBE tightened its monetary policy stance, increasing its main operation rate to 19.75% from 8.75% in February 2022. At its latest policy meeting in September, the CBE did not change its policy rates as inflation dynamics were broadly as it had expected.

Devaluation of the Egyptian pound will directly impact banks’ capital, inflating foreign currency risk-weighted assets. We think it is unlikely to directly harm banks’ asset quality, since foreign currency lending is at relatively low levels and is usually granted to companies that generate revenue in the same currency. However, under our base case, we still expect credit losses to increase due to the indirect impact of related increased production costs, as well as limited availability of foreign currency liquidity adding additional burden to sectors relaying on imports (see “For Egypt’s Banking Sector, The Economic Risk Trend Is Now Negative,” published on May 30, 2023). In addition, expanded lending to inherently riskier small and midsize enterprises (SMEs) will also contribute to asset quality deterioration. The CBE raised the threshold for SME lending to 25% of banks’ loan books on December 2022, from 20% previously, and set a new 10% minimum threshold for lending to small enterprises. We expect the banking sector’s pre-provision income to absorb the hit from increased loan loss provisions, thus not materially hindering capital. Banks’ increased reliance on external funding and limited access to foreign currency liquidity do, however, weigh on their funding profiles.