London – 11 Apr 2025:

Key Rating Drivers

Fundamental Rating Strengths and Weaknesses: The rating is supported by Egypt’s relatively large economy, fairly high potential GDP growth, and strong support from bilateral and multilateral partners. These factors are balanced by weak public finances, including exceptionally high debt interest/revenue, sizeable external financing needs and volatile commercial financing flows, high inflation and geopolitical risk.

Replenished External Buffers: External buffers have been preserved following the 1Q24 boost from the Ras El-Hekma foreign investment (underlining support from Gulf Cooperation Council (GCC) partners) and non-resident inflows into the domestic debt market. International reserves have risen by USD12.4 billion since early 2024, to USD45.5 billion in March 2025. The banking sector’s net foreign asset position (NFA) recovered sharply from a deficit of USD17.6 billion in January 2024 to a surplus of USD2.8 billion in June, before returning to a deficit of USD1.9 billion in February 2025. The weakening bank NFA position towards the end of 2024 coincided with moderate capital outflows, limiting currency depreciation.

Broadly Stable External Position Projected: Fitch forecasts the current account deficit to widen 0.2pp in FY25 (ending June 2025), to 5.6% of GDP, before narrowing to 4.0% in FY26, with only a gradual recovery in the energy deficit, helped by partial resumption of investment by international energy companies and the sourcing of lower-cost gas imports. Egypt has relatively limited direct exposure to US tariffs and cuts in US economic aid. We project FDI will rise to USD15 billion (3.8% of GDP) in FY26, boosted by new GCC real estate investment, and that international reserves end FY26 at 4.2 months of current external payments, from 5.1 in FY24, broadly in line with the ‘B’ median of 4.3 months.

Geopolitical Risk Still High: The main economic impact from ongoing regional conflicts is depressed Suez Canal receipts, which we project will only partially recover in FY26, to 60% of their 2023 level. Further escalation of conflict is a moderate risk to tourism revenue, which has been resilient, up 5% in FY24 and we project rises by 9% in FY26. Our base case remains that there is not a large influx of refugees from Gaza. Domestically, still high inflation, youth unemployment and weak governance pose lingering risks of greater social instability and alongside the widespread role of the military make economic reform challenging, in Fitch’s view.

More Flexible Exchange Rate: Greater exchange rate flexibility has been maintained since the March 2024 depreciation of the official rate, with no re-emergence of FX backlogs or a significant differential with the parallel market rate. In our view, FX demand management measures contribute to very low exchange rate volatility, but we do not consider significant currency misalignment has resulted. Nevertheless, in our view, the Central Bank of Egypt is not fully independent, the infrastructure for a fully-fledged inflation targeting regime is incomplete and a severe external shock would provide a greater test of commitment to exchange rate flexibility.

Relatively High Fiscal Deficit: Fitch forecasts the general government deficit widens by 4pp in FY25, to 7.4% of GDP, due to last year’s 3.3% of GDP one-off Ras El-Hekma revenue and high debt interest costs. This more than offsets lower capex, and strong tax revenue, which rose 38% in 8MFY25, helped by strengthening consumption, tax on government securities, reduced tax exemptions and improved compliance. The government plans an additional 1% of GDP in revenue measures in FY26, focussed on VAT, and we project it will come close to achieving this, contributing to a narrowing of the general government deficit, to 7.2% of GDP.

Risk from Off-Budget Spending: Despite steps taken over the last year to help contain off-budget spending, sizeable contingent liability risk remains from Egypt’s still-large and opaque broader public sector. Official data is not yet available on performance against the EGP1 trillion cap on overall public investment in FY25, but national accounts data indicates a significant slowdown. However, in Fitch’s view, there is uncertainty about the political durability of this commitment.

High but Falling Public Debt: Fitch projects general government debt falls to 80.4% of GDP at end-FY26, from 89.4% in FY24, still well above the projected ‘B’ median of 50.6%. We incorporate annual debt-enhancing, stock-flow adjustments averaging 1.5% of GDP, given Egypt’s record of off-budget spending. The government is now reporting fiscal performance at a broader level that incorporates 59 economic entities (which nearly halves the debt interest to revenue ratio), improving transparency, but Fitch has not adjusted its fiscal metrics to mirror this.

Inflation Falls Sharply: Inflation fell to 13.6% in March, from 24% in January (and 33.4% a year earlier), in line with our expectations, due to strong base effects, with core inflation at 9.4%. We project inflation rises to 14% at end-FY25, reflecting more fuel subsidy reductions (to reach full cost recovery by January 2026), before falling to 10.5% at end-FY26, on broad exchange rate stability and better anchored inflation expectations, still well above the current ‘B’ median of 4.5%.

Extreme Debt Interest to Fall: Fitch anticipates the policy interest rate, which has been held at 27.25% since March 2024, is cut to a level consistent with a real rate of near 4% by end-FY26, underpinning a rapid fall in debt interest costs (given the average maturity of domestic debt is under two years). We forecast general government debt interest/revenue (which is lower than at the central government level) falls from a peak of near 61% in FY26, to 38% in FY29, but still more than three times the current ‘B’ median of 12%.

Growth to Accelerate, Moderate Reform: Fitch forecasts real GDP growth accelerates to 4.0% in FY25, from 2.4% in FY24, helped by recovering confidence, and to 4.7% in FY26, on strengthening real income growth, albeit slightly below the potential growth rate. The government is firmly committed to the IMF programme, which has focussed on restoring macro-fiscal stability. However, there has been more limited structural reform to boost competitiveness and avoid the re-emergence of external imbalances into the medium term. Progress includes tax system rationalisation, reduced state-owned enterprises tax exemptions and improved customs processes, whereas state divestment has been modest.

Resilient Banking Sector: Egypt’s large and liquid banking sector provides financing flexibility for the sovereign, with a low loan-to-deposit ratio of 62.5% at end-2024. Fitch anticipates strong deposit growth and that banks deploy most of this liquidity in government securities. We anticipate the common equity Tier 1 ratio, which has recovered to 12.7%, improves further on internal capital generation, and that net profit growth normalises this year to 30%-50%, after a rise of 89% in 2024.

ESG – Governance: Egypt has an ESG Relevance Score (RS) of ‘5’ for both Political Stability and Rights and for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption. These scores reflect the high weight that the World Bank Governance Indicators (WBGI) have in our proprietary Sovereign Rating Model (SRM). Egypt has a low WBGI ranking at the 28th percentile, with a particularly low score for voice and accountability.

RATING SENSITIVITIES

Factors that Could, Individually or Collectively, Lead to Negative Rating Action/Downgrade

– External Finances/Macro: Deterioration in external finances and/or confidence in macro-policy settings, for example, as a result of a weaker commitment to exchange rate flexibility, weaker international reserves and bank net foreign asset positions, a sustained large current account deficit and more constrained access to external financing.

– Public Finances: Increased debt sustainability risks, for example, as a result of loosening of fiscal policy, failure to bring down interest/revenue and government debt/GDP in the medium term, or weaker financing flexibility.

– Structural Features: A further escalation of regional conflict increasing instability and security risk in Egypt, with a larger negative spill-over impact on tourism, Suez Canal receipts, investor sentiment, or increasing the domestic socio-political challenge to implementing reforms.

Factors that Could, Individually or Collectively, Lead to Positive Rating Action/Upgrade

– External Finances: Further reduction in external vulnerabilities, for example, through a marked strengthening of the international reserve position, a sustainable narrowing of the current account deficit, structural reform that reduces risks of renewed imbalances, and improved international market access.

– Macro/External: Greater confidence in the durability of policy adjustments to support exchange rate flexibility and a marked fall in inflation closer to target.

– Public Finances: Lower debt issuance costs, and fiscal consolidation, potentially through greater revenue mobilisation and containment of off-budget spending, that sharply reduce debt interest/revenue and put public debt/GDP on a firm downward path over the medium term.

Sovereign Rating Model (SRM) and Qualitative Overlay (QO)

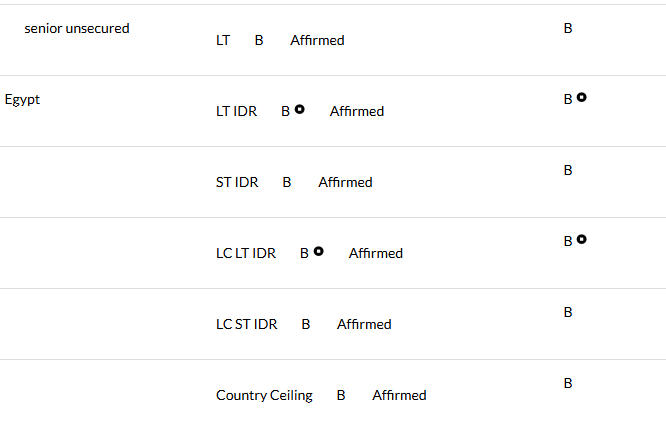

Fitch’s proprietary SRM assigns Egypt a score equivalent to a rating of ‘B-‘ on the Long-Term Foreign-Currency (LTFC) IDR scale.

Fitch’s sovereign rating committee adjusted the output from the SRM to arrive at the final LTFC IDR by applying its QO, relative to SRM data and output, as follows:

– Macro: +1 notch, to reflect a material improvement in macro-policy settings that underpin expectations for lower macroeconomic instability, in particular reduced distortions in the FX market and a marked fall in inflation, which is not yet fully captured in the SRM.

Fitch’s SRM is the agency’s proprietary multiple regression rating model that employs 18 variables based on three-year centred averages, including one year of forecasts, to produce a score equivalent to a LTFC IDR. Fitch’s QO is a forward-looking qualitative framework designed to allow for adjustment to the SRM output to assign the final rating, reflecting factors within our criteria that are not fully quantifiable and/or not fully reflected in the SRM.

Country Ceiling

The Country Ceiling for Egypt is ‘B’, in line with the LTFC IDR. This reflects no material constraints and incentives, relative to the IDR, against capital or exchange controls being imposed that would prevent or significantly impede the private sector from converting local currency into foreign currency and transferring the proceeds to non-resident creditors to service debt payments.

Fitch’s Country Ceiling Model produced a starting point uplift of 0 notches above the IDR. Fitch’s rating committee did not apply a qualitative adjustment to the model result.

REFERENCES FOR SUBSTANTIALLY MATERIAL SOURCE CITED AS KEY DRIVER OF RATING

The principal sources of information used in the analysis are described in the Applicable Criteria.

ESG Considerations

Egypt has an ESG Relevance Score of ‘5’ for Political Stability and Rights as WBGI have the highest weight in Fitch’s SRM and are, therefore, highly relevant to the rating and a key rating driver with a high weight. As Egypt has a percentile rank below 50 for the respective Governance Indicator, this has a negative impact on the credit profile.

Egypt has an ESG Relevance Score of ‘5” for Rule of Law, Institutional and Regulatory Quality and Control of Corruption as WBGI have the highest weight in Fitch’s SRM and are therefore highly relevant to the rating and are a key rating driver with a high weight. As Egypt has a percentile rank below 50 for the respective Governance Indicators, this has a negative impact on the credit profile.

Egypt has an ESG Relevance Score of ‘4’ for Human Rights and Political Freedoms as the Voice and Accountability pillar of the WBGI is relevant to the rating and a rating driver. As Egypt has a percentile rank below 50 for the respective Governance Indicator, this has a negative impact on the credit profile.

Egypt has an ESG Relevance Score of ‘4+’ for Creditor Rights as willingness to service and repay debt is relevant to the rating and is a rating driver for Egypt, as for all sovereigns. As Egypt has a track record of 20+ years without a restructuring of public debt and captured in our SRM variable, this has a positive impact on the credit profile.

The highest level of ESG credit relevance is a score of ‘3’, unless otherwise disclosed in this section. A score of ‘3’ means ESG issues are credit-neutral or have only a minimal credit impact on the entity, either due to their nature or the way in which they are being managed by the entity. Fitch’s ESG Relevance Scores are not inputs in the rating process; they are an observation on the relevance and materiality of ESG factors in the rating decision. For more information on Fitch’s ESG Relevance Scores, visit.