Cairo 16 Mar 2024ö

The UAE’s investment in the Ras al Hekma project on Egypt’s north coast, Followed soon after by the flotation of the Egyptian Pound, a hike in interest rates and the signing of a staff level agreement with the IMF for an augmented extended fund facility, has dramatically changed Egypt’s medium-term financing outlook since our most recent update in early February. In this CEEMEA in Focus, we present our updated projections and highlight what we think are the key changes to the external financing outlook implied by these recent developments.

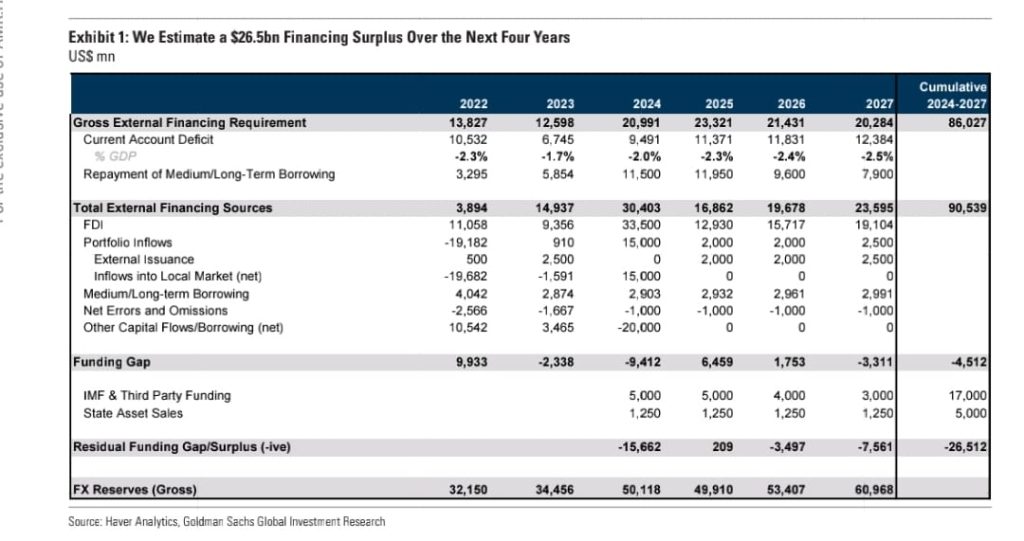

A much stronger pipeline of external funding sources, combined with a larger funding package from the IMF and partners, will mean a surplus of external funding to the tune of $26.5bn over the next four years, according to our projections. This compares favourably to our projection of a funding deficit of $13bn prior to the recent developments.

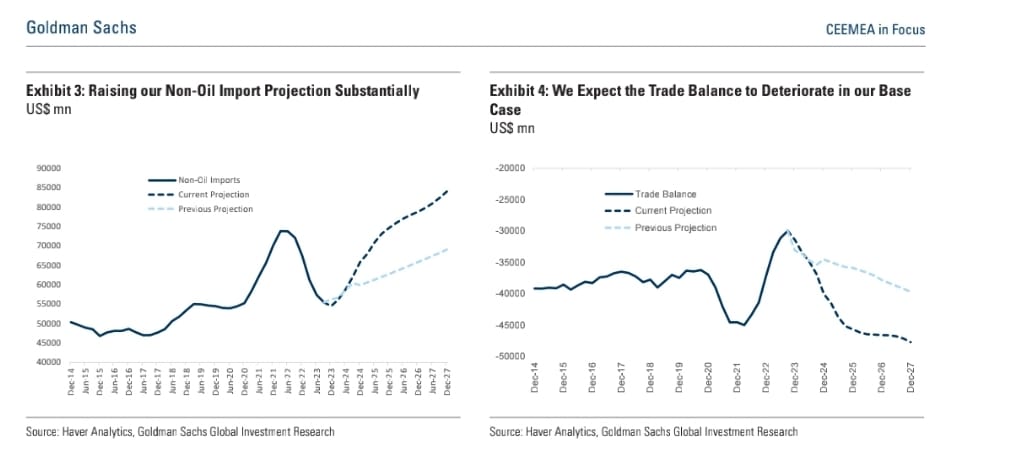

We expect the current account deficit to widen relative to our previous projections as imports rise at a faster pace and are only partially offset by an increase in worker remittances. We see the deficit widening to 2.5% of GDP by

end-2027.

The widening current account deficit should be more than offset by stronger capital inflows. FDI this year alone is likely to reach over $33bn, and is likely to rise faster than we had been anticipating as the macro backdrop stabilises and investment in new projects picks up. We also see a return of portfolio inflows this year, mainly in the local market (carry trade).

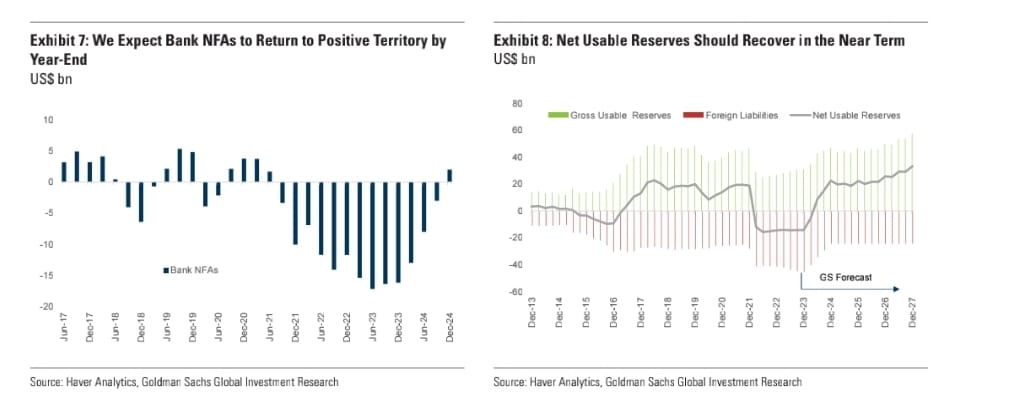

All this should lead to a considerable strengthening in external buffers. We project gross FX reserves to rise to over $60bn by end-2027, and an even greater increase in net reserves as GCC deposits at the central bank are converted into equity in new projects. We also see bank NFAs returning to a flat position by the end of this year.

At the beginning of February, we published an update of our estimates for the external funding needs and sources for Egypt, projecting a funding gap (post-IMF) of $13bn, which we suggested could be filled with asset sales and alternative external financing.

The UAE’s investment in the Ras al Hekma project on Egypt’s north coast, followed soon after by the flotation of the Egyptian Pound and the signing of a staff level agreement with the IMF for an augmented extended fund facility, has dramatically changed the financing outlook. In this CEEMEA in Focus, we present our updated projections and highlight what we think are the key changes to the external financing outlook implied by these recent developments.

From $13bn Deficit to $26.5bn Financing Surplus

In Exhibit 1 we present our updated headline projections for Egypt’s external financing needs and sources. Our estimate for the overall financing requirement (current account deficit plus amortisation of medium- and long-term external debt) has risen relative to our previous update in early February as we expect the current account deficit to widen modestly as a result of recent developments (see below). That said, a much stronger pipeline of external funding sources combined with a larger funding package from the IMF and partners will mean a surplus of external funding to the tune of $26.5bn over the next four years, according to our projections. This compares favourably to our projection of a funding deficit of $13bn prior to the recent developments.

The Current Account Deficit Likely to Widen Modestly Details of our current account projections are presented in Exhibit 2. We are forecasting that the current account deficit will widen steadily from an estimated 1.7% of GDP in 2023 to around 2.5% of GDP over the next four years. This is a significant revision to our previous forecasts, which had projected the deficit to narrow to 1.5% of GDP by end-2027.

The key drivers of the changes to our forecasts are as follows:

Trade deficit widening: While the depreciation of the official exchange rate may prima facie argue for some competitive boost and a narrowing of the trade balance,

we think the opposite is true because:

– There has been no effective depreciation in the currency given the

infra-marginalisation of the official rate and the ubiquitous use of the parallel

rate for FX transactions over the past two years.

-We believe the currency will continue to strengthen in the coming weeks and

months on the back of strong FX inflows.

-The greater availability of FX should ease a major constraint on import growth.

-An increase in foreign investment (particularly in the real estate sector) is

likely to boost domestic demand in the medium term.

-We are also projecting strong export growth (as access to raw materials and

imported components improves) but this would only partially offset import growth given the smaller magnitude of exports.

We show our updated import growth path (relative to our previous projections) in Exhibit 3, and the revised trade deficit trajectory in Exhibit 4.

Rise in workers’ remittances should partially offset widening in trade deficit:

We had previously been projecting a gradual return of workers’ remittances, reaching just under $30bn by end-2027. The greater-than-expected devaluation of the Pound, higher rates and stronger growth outlook all lead us to believe that remittances will return faster and in greater size, offsetting much of the widening in the trade deficit.

Accounting for FX backlog: Prior to the devaluation, estimates of the FX backlog ranged from $5bn to $10bn, according to our local banking contacts. Local banks have begun clearing this backlog in recent days, and we assume that around $7bn in FX will ultimately be expended for this purpose this year. This outflow is reflected in our numbers, as an increase in either current account payments or capital account outflows.

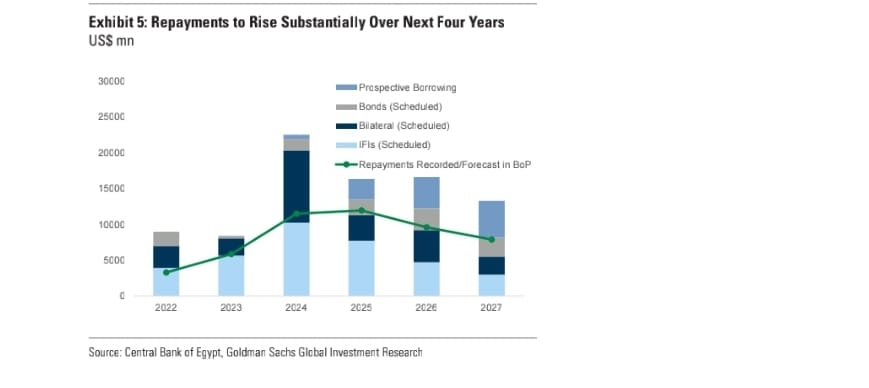

No Change to our Debt Repayments Schedule

We have not made any changes to our amortization schedule following the recent developments. The additional capital inflows relative to our previous projections are mainly FDI or official sector borrowing (IMF and partners), repayment of which will begin

beyond the forecast horizon. We present our (unchanged) assumptions for the repayment of medium- and long-term debt over the next four years in Exhibit 5.

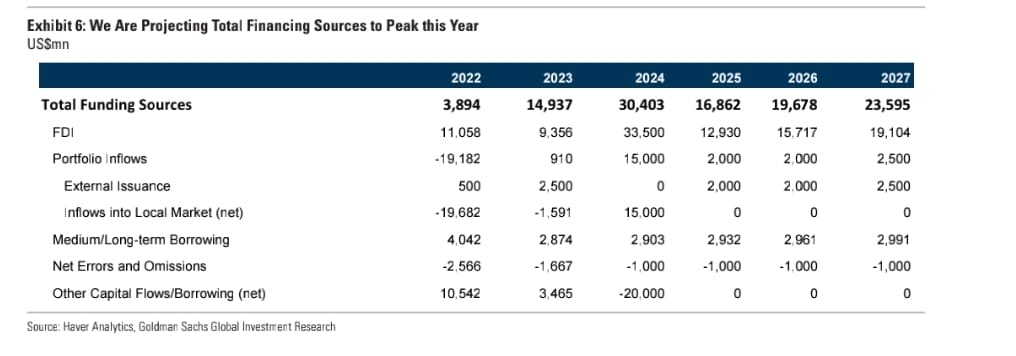

Capital Account Inflows Set to Rise Sharply In our view, the recent developments will have a profound impact on the prospect for capital account inflows over the coming years.

The breakdown of these inflows is presented in Exhibit 6, and includes:

A sharp rise in FDI inflows: The Ras al Hekma deal alone will add $24bn to FDI inflows this year (the net amount being paid by the UAE from external resources).

We add this to our previous baseline of around $9bn in FDI inflows in 2024. While we expect more such deals with other Gulf partners to materialise in the near term, we are conservatively assuming that these will be financed with internal resources

(deposits with the CBE), which would have a positive impact on the net reserve position of the CBE (see below) but not bring additional inflows into the country.

That said, from next year onwards, the stabilising macro backdrop, easing of currency concerns and expected investments in Ras al Hekma and other similar projects should see FDI rise significantly above our previous baseline of $9bn, reaching over $19bn by 2027 according to our projections.

A return of portfolio inflows this year: Our previous base case envisioned a modest pick-up in portfolio inflows over the next four years. The devaluation/overshoot of the Pound and the hike in rates have catalysed strong interest in the carry trade, and we now project around $15bn of net inflows this year, before leveling off next year and beyond. With respect to external issuance, we do

not include any for this year but see a return to markets from next year, with around $2bn in annual issuance across all markets.

A near-term rise in ‘other’ capital outflows: We are penciling in $20bn in ‘other’ capital outflows this year, $2bn of which is the capital account contribution to the clearing of the FX backlog (as mentioned earlier), and $18bn of which represents the rehabilitation of the banks’ NFA position (increase in foreign assets, decrease in foreign liabilities).

Monetary Reserves to Rise in Our Base Case

The increase in FX inflows will more than offset the rise in external funding needs over the next four years, in our view, leading to a strengthening in FX buffers as follows:

Balance in bank NFAs should be restored: As mentioned above, we assume $18bn in capital outflows this year as banks increase their foreign assets and reduce their foreign liabilities in order to repair their external balance sheets. We think this will lead to a balanced NFA position by the end of this year (Exhibit 7).

Official FX reserves to increase: Our projections imply an increase in gross FX reserves to around $61bn by end-2027 (Exhibit 1). On a net basis, the increase should be even greater as we assume that the conversion of GCC deposits to equity in domestic projects reduces CBE liabilities by $21bn ($11bn announced for the Ras al Hekma deal, and we assume a further $10bn for similar deals this year).